SWITCH SECTION

SWITCH SECTION

The German cost problem prevents medium-term recovery in residential construction

The German cost problem prevents medium-term recovery in residential construction

EUROCONSTRUCT. Briefing on European construction October 2024.

EUROCONSTRUCT. Briefing on European construction October 2024.

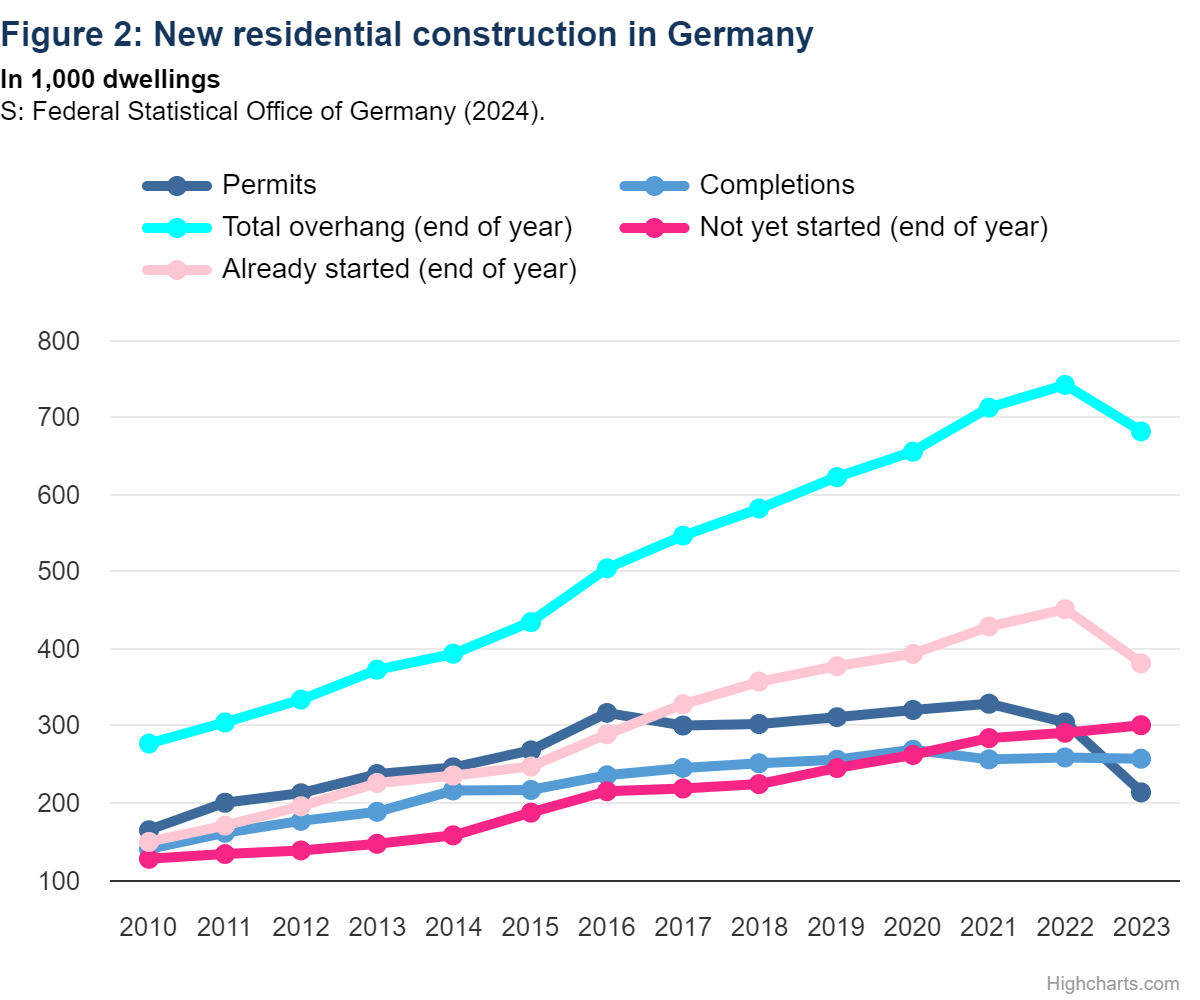

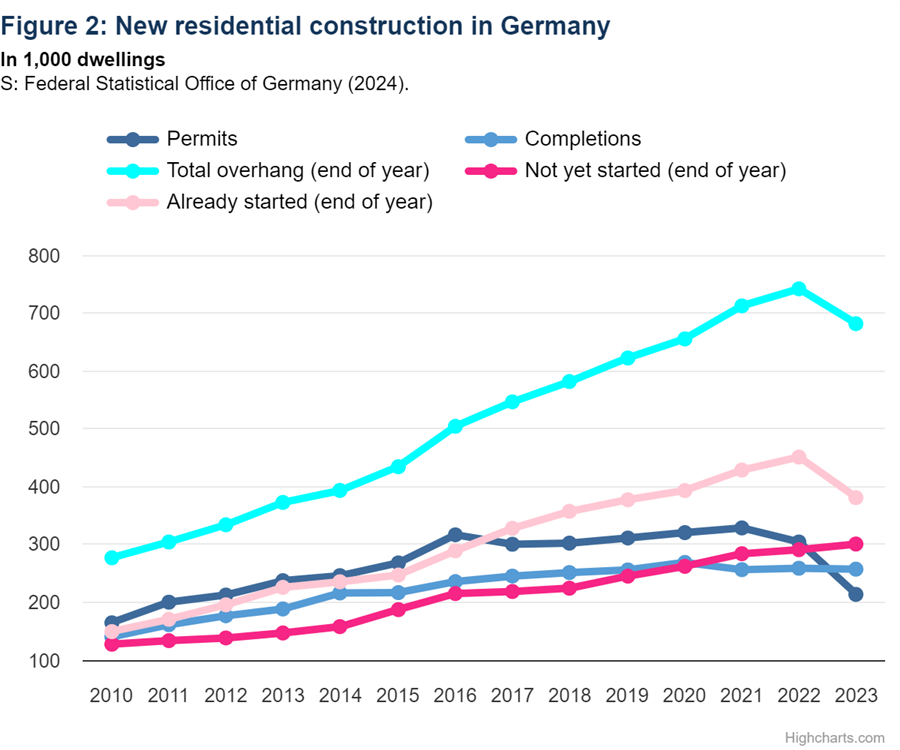

The German construction industry is suffering from excessively high construction costs. This has negative consequences for new residential construction in particular. While many private households are already struggling to cope with the sharp rise in consumer prices, the development of construction costs is clearly overshadowing the latest wave of inflation. The project pipeline is emptying as the number of building permits falls, but due to the long construction times, the completion figures were still stable until 2023. However, their pronounced downward slide will already begin this year.

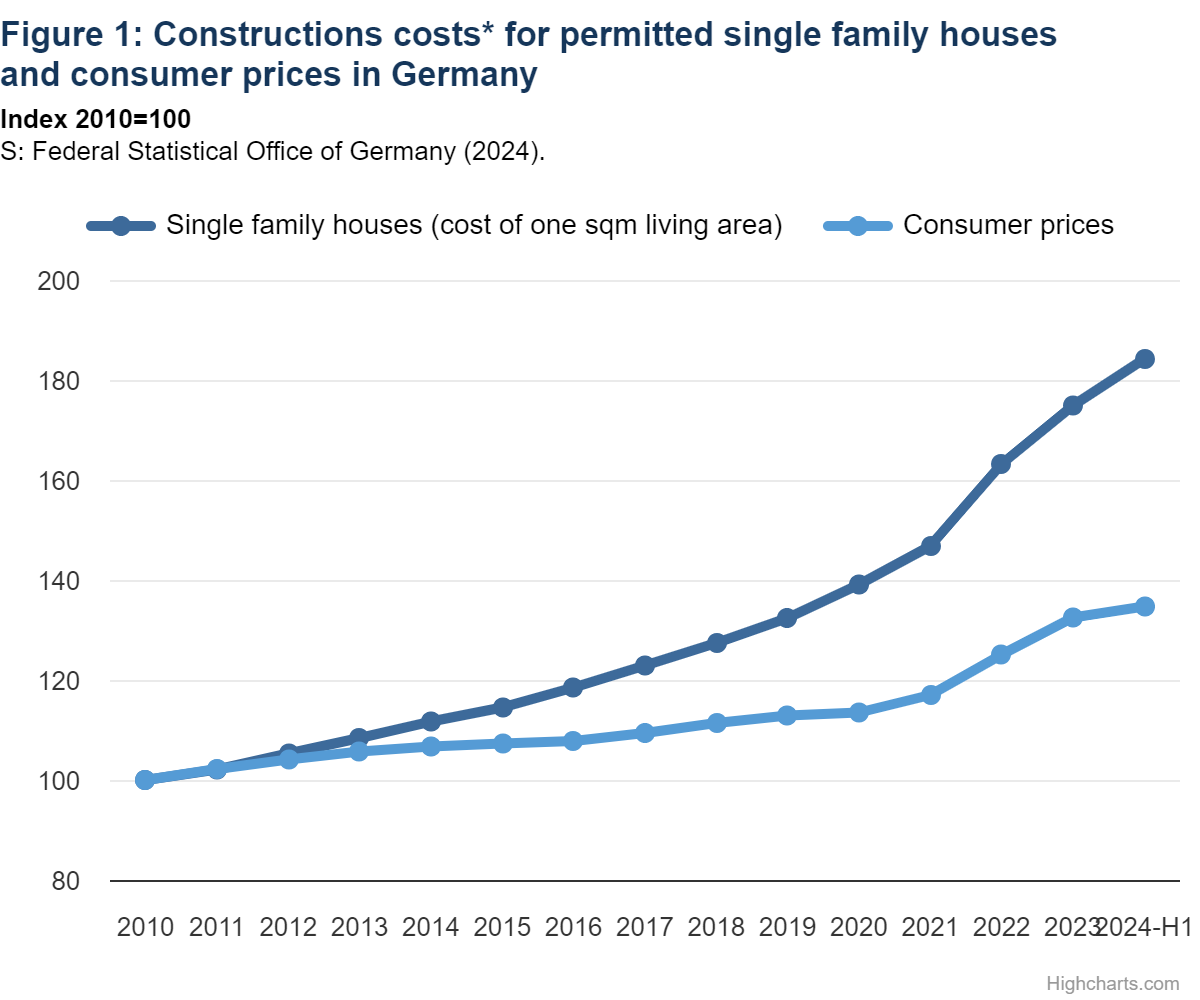

The construction of new buildings in Germany has become much more expensive in recent years. According to official statistics on building permits, the construction of a single-family home cost an average of around 200,000 euros in 2010. This figure includes the originally planned expenditure for the building (building structure and technical systems) itself, but not the costs for the plot or its development, for the outdoor facilities/open spaces, for fitted kitchens and ancillary costs such as expenses for planning or financing. At that time, the calculated cost per square metre of living space for the building alone was around 1,360 euros. In the first half of 2024, the figure was 2,510 euros per square metre or just under 390,000 euros per building with the living space increasing from 147 to 153 square metres. In short, this enormous increase of more than four-fifths is primarily due to the tightening of countless building regulations and the explosion in construction prices (e.g. due to material costs) in the wake of the recent crises and in part to the increased demands of users. Almost only wealthy private households can now afford a new single-family house, and they don’t have to pay attention to the last euro when it comes to design and fittings.

“The risen interest rates should not be used as a permanent argument for the weak construction demand.”

According to official approval statistics, the average cost of living space in single-family house construction rose by 84% between 2010 and the first half of 2024, compared to even 94% in multi-family house construction. However, consumer prices only increased by a good third in the same period. The sharp rise in construction costs does not stop at prefabricated residential construction or non-residential building construction, and is therefore largely responsible for the general reluctance to build. The turnaround in interest rates, on the other hand, should not be used as a permanent argument for the weak demand for construction, as interest rates have now returned to a ‘normal’ level. The federal government’s subsidisation of new construction, which has now been reduced to a minimum, is creating headwinds, as is the – at least slowly decreasing – loss of purchasing power among private households. However, the German new construction sector, and new residential construction in particular, has a cost problem above all. Current political endeavours (e.g. building type E) are unlikely to bring about a turnaround in new residential construction and thus significantly mitigate the ongoing crash.

The stable development of housing completion figures in 2023 belies the ongoing market contraction. For example, approvals for new residential buildings registered in 2023 were already 115,000 residential units lower than in 2021. For this reason, the so-called construction overhang (all approved but not yet completed dwellings) fell noticeably to 682,000 units by the end of 2023. At 380,000 units, there were 70,000 fewer under construction than at the end of 2022. At the same time, the number of dwellings not yet started (whose building permit has not expired) increased by 10,000 to just over 300,000 residential units, possibly also due to cost uncertainties.

“The number of dwellings not yet started increased further, although approvals fell significantly.”

Not only are the supplies slowing down, but fewer and fewer projects are actually being realised. In 2024, only 170,000 dwelling permits for new residential buildings (of which 50,000 for single and two-family houses) are likely to be received and the number of completions will fall to around 215,000 residential units (of which 70,000 in single and two-family houses). By 2026, however, only around 145,000 units are likely to be built in new single- and two-family houses and in new multi-family buildings (including residential homes). Together with the expected ca. 30,000 further completions in existing buildings and in new non-residential buildings, this results in a total completion number of just 175,000 dwellings for 2026.

Texten är skriven av Ludwig Dorffmeister, analytiker på Ifo Institute. Ifo Institute är Tysklands representant i det europeiska analysnätverket EUROCONSTRUCT.

Läs mer om Euroconstruct här eller ta kontakt med oss om du är intresserad av bygg- och anläggningsprognoser för de europeiska marknaderna.